Investment is a buzz word we hear everywhere in recent days. Investing helps to secure a better future for individuals and families. In Nepal, options like stocks, fixed deposits, real estate, gold, mutual funds, and government bonds offer varying returns over time. Over the last five to six years, Nepal’s investment landscape has transformed dramatically, due to pandemic and digital platforms.

Performance Over the Last 5–6 Years

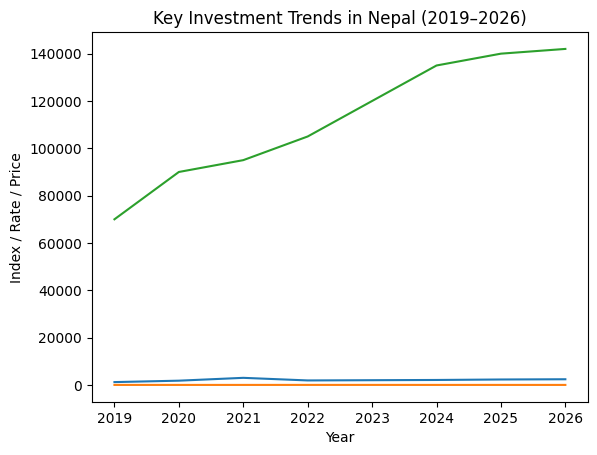

Figure: Trend comparison of NEPSE index, fixed deposit rates, and gold prices in Nepal (2019–2026).

Nepal’s investments have seen cycles of highs and lows. During the 2020–2021 pandemic, the Nepal Stock Exchange (NEPSE) index surged to record highs above 3,000 points, driven by low interest rates. However, policies like the 2/12 crore loan limit and rising interest rates triggered a crash, dropping the index below 1,900 by late 2022.

Real estate boomed post-pandemic, with land prices along Kathmandu’s Ring Road doubling or tripling in prime spots due to remittance inflows. Fixed deposit (FD) rates peaked at 13–15% in 2022–2023 amid liquidity crises but fell to 6–8% by early 2026 as Nepal Rastra Bank (NRB) eased rates. Gold prices rose steadily, hitting new highs around NPR 140,000 per tola in 2025, outpacing inflation.

Mutual funds and government bonds offered steadier but modest returns (8–12% annualized), while stocks revived modestly in 2025–2026 with hydropower and banking sectors leading.

Descriptions of Key Investment Options

Fixed Deposits: These involve depositing funds in banks or finance companies for 3 months to 5 years. It offers moderate liquidity and early withdrawal incurs penalties. It is like a locked piggy bank and can help you get steady coins. Returns track NRB rates, peaking during tight liquidity but now cooled to 6–8%. Low credit risk in insured strong banks made them a safe haven during NEPSE volatility and pandemic uncertainty, though they lag for long-term wealth building.

Stocks: Stocks are shares and ownership of listed companies like banks, hydropower, insurance, microfinance, and manufacturing via NEPSE. High returns during bull runs (e.g., 2021), but extreme volatility, sector concentration (finance/hydropower dominate 70%). It is risky as it changes with policies.

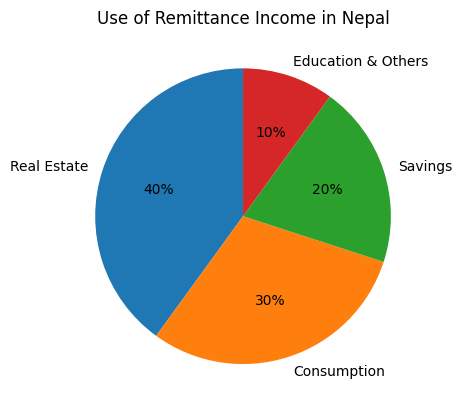

Real Estate: Residential/commercial properties or land plots, especially urban/semi-urban. Strong wealth builder with 15–25% annual appreciation in prime areas. In Nepal, people spent more money on real estate. For instance, about 40% of remittance is spent on acquiring real estate. It has low liquidity as it is hard to sell quickly and vulnerable to NRB policy crashes.

Gold: A hedge against inflation, with prices climbing to new highs. Moderate returns (10–15%), high liquidity, but no income generation and storage/security costs.

Mutual Funds: Professionally managed pools investing in equities, bonds, and deposits; SIPs enable monthly small investments. Balanced returns (10–14%), lower volatility than direct stocks, good for beginners.

Government Bonds: Government bonds are money lent to the government , It is a safest bet as it has fixed pay. Government bonds mature in months to 10 years. It has low risk, low return.

Current Trends in Nepal

Nepalis are shifting toward digital and diversified options like SIPs in mutual funds, driven by easier access via apps and NEPSE revival in hydropower. Real estate claims 40% of remittances for urban plots, prized for tangible value and appreciation despite illiquidity. Fixed deposits have lost appeal with cooling rates and improved liquidity.

Stocks are reviving post-2024 lows, attracting young investors amid economic recovery. Gold remains popular for cultural hedging. Overall, risk tolerance is rising, but caution lingers from past crash remittances and NRB policies heavily influence flows.

Figure: Distribution of remittance income usage in Nepal.

Making Informed Investment Decisions

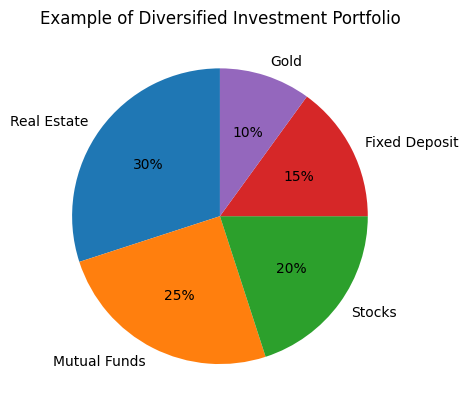

Historical data shows diversification beats single-asset investment. Therefore we need to analyze and plan our investment. As an individual, one needs to track NRB rates and allocate budget into real estate, mutual fund, stocks and FD. One can be more aware about policies and take consultation from experts. If you are new you can ask help from various agencies and start investing.

Figure: Illustrative diversified investment portfolio for Nepali investors.